Best Way to Invest Cash

A reader recently asked what to do with several hundred thousand dollars that he received when he sold his tech stocks.

What a great problem to have, you come into $100,000, $500,000 or more, in cash and you’re wondering how to invest it.

Investing large sums of money into the stock market all at once can be frightening, especially now, when the stock market is overvalued. It’s a well-known tenet that when stock prices get ahead of their underlying value, at some point, those prices will fall back in line with the company’s valuation. But here’s the catch, stocks can remain overvalued for years, and years.

Contents [hide]

- Best Way to Invest Cash

- Price Earnings Ratio

- How to Invest a Cash Windfall, if I Will Need the Money within the Next Five Years?

- Here’s where to invest cash that you’ll need within the next five years:

- How to Invest Large Sums of Money for the Future

- When to Reinvest a Large Amount of Money – Lump Sum or Dollar Cost Average?

- What to do With a Financial Windfall – Wrap Up

- Related

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

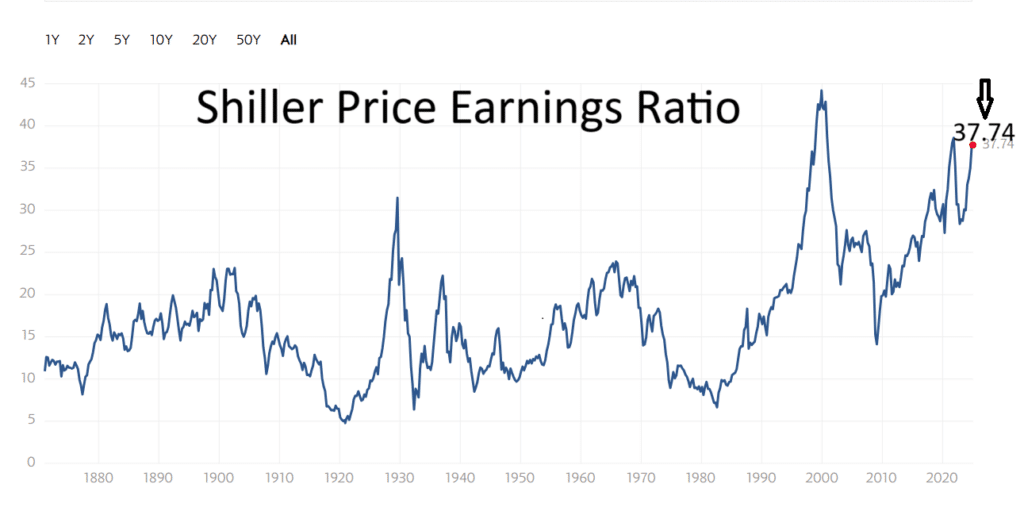

Price Earnings Ratio

source: Shiller PE Ratio – Multpl

The average Shiller PE ratio is 17.19, in contrast with the January 2025 PE ratio of 37.74. According to this metric, the S&P 500 is overvalued by roughly 100%. No wonder, the reader is concerned about reinvesting his windfall into the stock market today. What if he invests $100,000 or more into the stock market today and within the year, the stock market takes a tumble and falls 20%. His $100,000 is then worth $80,000.

Here are the steps to take when considering “How to invest $100,000 or more.”

Questions to ask before investing large amounts of money in the stock market:

- Will I need the money soon, within the next few years?

- How would I feel if I invested the money in the stock market today, and next month the market dropped 20%?

- Can I leave the money invested in the stock market for seven years or more?

Keep your answers in mind, as you review the article and watch the YouTube video below.

Next we’ll explore how to invest a cash windfall in the stock or when to invest a cash windfall in a high yield liquid asset.

How to Invest a Cash Windfall, if I Will Need the Money within the Next Five Years?

If you are wondering the best way to invest a cash windfall but will need the money within the next few years, then your answer is simple. Any money you’ll need within the next one to five years should not be invested in the stock market. The reason is that the stock market is volatile and could decline precipitously at any time.

If you’re planning a large home remodel, buying a new car for cash or buying a home and need a large down payment, then don’t put your cash windfall into the stock market! The risk of loss, is too great. Here’s the best way to invest cash short term.

The key to short term investing is to make certain that the principal value remains steady and funds are liquid. This means you’ll trade the potential for higher stock market returns, for the likelihood that your cash will be there when you need it.

Here’s where to invest cash that you’ll need within the next five years:

High yield cash account. Many investment platforms, like M1 Finance and Wealthfront offer cash accounts with no management fees and above average yields.

Money Market Mutual Fund. A money market mutual fund is purchased through your investment broker and owns short term debt, is liquid, maintains a one dollar per share value and typically pays a monthly dividend, which is higher than the return you’ll get from your bank savings account.

Certificate of Deposit or CD. Purchased through your bank or investment broker, these cash-equivalent assets come in various terms from several months up to five years or so. They pay a higher interest rate than your bank savings account. You’ll pay a small penalty (usually 3 months interest) if you cash the CD in early.

If you won’t need your cash for the next five years or so, and want to invest it for the future, like retirement or college for your toddler, then the stock market is usually a good choice.

How to Invest Large Sums of Money for the Future

If you’re saving for retirement or goals that are ten years or more into the future, the stock market is a good place to grow your wealth. Over the past hundred years or so, the historical stock market returns have averaged around 9% per year. After all, you’re putting your money into growing companies within the U.S. and across the globe.

In the short term, the stock market returns are uncertain, but over the long term, returns have trended upwards. But, despite a long-term perspective, make sure that you can withstand periodic downturns in the market. If you are a long-term investor, you do not want to sell stock market investments after the stock market declines. That is the best way to lose money in the long run. The reason it’s best for long-term investors to stay in the market, even after a decline, is because, the market can reverse course fast, before you have a chance to reinvest the funds that you withdrew.

If you sell at the bottom, you have to be right twice, once when you sell, and again when you reenter the market. And that’s very difficult to accomplish.

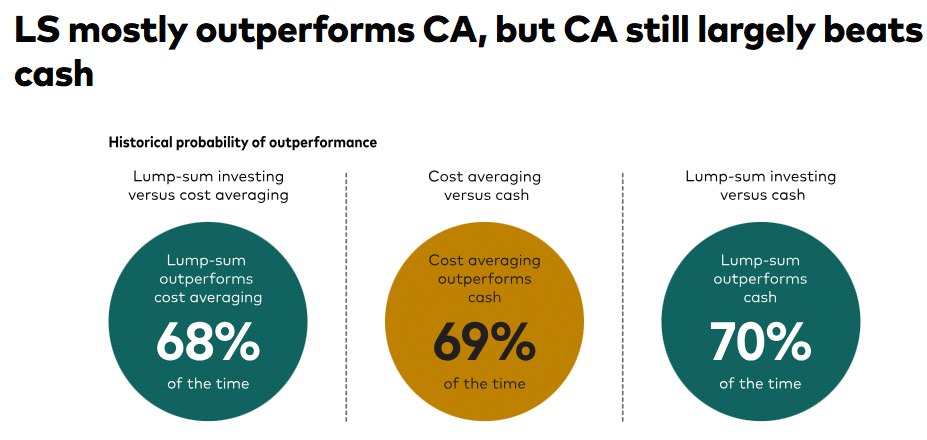

Source: https://investor.vanguard.com/investor-resources-education/news/lump-sum-investing-versus-cost-averaging-which-is-better

When to Reinvest a Large Amount of Money – Lump Sum or Dollar Cost Average?

A recent Vanguard research article found lump sum investing (LS) tends to outperform dollar cost averaging (CA), over the long term. But that might not be the best alternative for you.

When the markets are highly valued, dollar cost averaging your cash into the market might be the best way to go, if you believe the stock market is ready for a decline. Dollar cost averaging is an investment strategy that recommends investing specific amounts of money into the market, at regular intervals. For example, your monthly 401k or retirement contributions, are dollar cost averaging your annual retirement plan monies into the market in regular dollar value installments. When markets are highly valued, you’ll buy few shares. When values decline, your steady dollar amount will buy more shares, at a lower cost.

The disadvantage of dollar cost averaging is the lost opportunity cost of the money, should the stock market increase in value. In a rising market, it’s best to invest all at once, while in a declining market, dollar cost averaging will yield greater returns.

Unfortunately, no one knows if the market will go up or down during the near term. Although long term trends support a rising stock market. That’s why in long term research, lump sum investing outperforms dollar cost averaging.

The image above shows that lump sum investing outperforms dollar cost averaging 70% of the time vs 68% of the time for dollar CA.

The middle chart reminds long term investors, that investing in the markets will yield higher returns than leaving the funds in cash! Dollar cost averaging beats cash investing 58% of the time. Unless you’re in or near retirement, or will need your cash within the next few, stay in the financial markets.

What to do With a Financial Windfall – Wrap Up

After receiving a financial windfall – take a breath. No need to make a decision immediately. If you lack investment knowledge, learn about investing and the financial markets. One of my favorite investment books is the 100 page “Elements of Investing”, by Malkiel and Ellis. You can also learn investing basics with my free micro-book, “How To Invest And Grow Your Wealth.”

If you need your money within the next several years, or part of it, then that money should be invested in short-term cash investments.

Long term money should be invested in a diversified portfolio of stock investments. Here are some articles to help you invest your money:

- How To Create A Diversified Index Fund Portfolio

- Lazy Investors Asset Allocation Guide to Amass $787, 355

- Best Lazy Portfolios For Wealth Building

Finally, congratulations on your cash windfall. Invest wisely, and your money can grow and compound handsomely for the future.

Free-How to Invest & Grow Your Wealth

We respect your email privacy

Related

- How Much Cash Should I Have On Hand?

- The Secret To Flawless Investment Management – FREE

- Where To Invest In An Overvalued Market?

- Which Investments Carry The Least Risk?

- How To Get A Good Return On Your Cash

- What Is A Good Investment Return?

- Do I Need A Financial Advisor?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

M1 Disclosure: This content is not a solicitation, is not endorsed by M1, and was not reviewed by M1; the opinions expressed are solely those of the authors and do not reflect M1’s views. Information presented is accurate as of the video posting date; for the most up-to-date information, please refer to m1.com. Before making any investment decisions, consult your personal investment, legal, and tax advisors, as this content is for informational purposes only and not intended as investment recommendations.

*M1 Promotion Period: December 30, 2024 – January 31, 2025 – see conditions https://m1.com/legal/disclosures/afiliate-jan-2025-earn-apy-boost-tc/

Read the full article here